Don spent much of his career helping clients turn Debt & Taxes into Savings & Investment™. Today he serves roughly 95 clients, most of whom are retired or close to it. As he approaches the twilight of his career, his primary aim is to help clients discover new opportunities and create possibilities not previously imagined.

“It’s the economy, stupid” is a phrase widely used during Bill Clinton’s 1992 presidential campaign. Generally attributed to Clinton political strategist James Carville, the phrase is often repeated in American political culture, with commentators sometimes using a different word in place of “economy”. But whether it’s the deficit, the voters, or the environment(stupid!) you substitute for economy, the phrase is meant to focus attention upon what matters most in the world of politics.

Retirement needs are so often expressed in terms of income (with many experts recommending replacing 70-80% of ones pre-retirement income), you might think income is what matters most in the world of retirement planning.

Unfortunately, this can lead people to conflate income with spending, and the mistaken belief that 70-80% of pre-retirement income is recommended because a 20-30% decline in post-retirement spending is the norm.

What the rule of thumb is actually attempting to convey is the average amount of pre-retirement income not being used to fund pre-retirement spending.

While some pre-retirement income is spent on things like clothing, dry cleaning or commuting expenses – post paycheck spending that will be reduced, or even vanish in retirement – these kinds of expenses tend to be minor compared to payroll deductions like 401(k) contributions, pension obligations, and Social Security taxes.

All of this is to say that the recommendation to replace 70-80% of pre-retirement income is not meant to suggest your post-retirement spending will be any less than it is today.

In fact, hopefully your post-retirement spending on things like food, utilities, entertainment, etc., is every bit as much as it was before you retired!

Who wants to limit their consumption of food, utilities or entertainment to 70-80% of what it was before retirement? In assessing your retirement needs it’s best to target (100% of) your spending rather than (70-80% of) your income. Because when it comes to retirement planning – it’s the spending, stupid!

Working for yourself has its perks. In theory there’s more autonomy when you’re calling the shots. But that autonomy often comes at a cost. Taxes can be particularly burdensome on the self-employed. And the recent Tax Cut and Jobs Act of 2017 (TCJA) re-shuffles the deck on many age-old tax strategies. Navigating the effects of the TCJA is something everyone will need to do. But for self-employed professionals, TCJA offers both threat and opportunity.

The TCJA created a new species of taxpaying entity known as a Specific Service Trade or Business (SSTB). Along with a new category of income called Qualified Business Income (QBI), and corresponding QBI deduction.

Unfortunately for most SSTBs, this new QBI deduction begins to be phased-out for married filers at 2018 taxable incomes of $315,000 ($157,500 for single filers). For 2019, these phase-outs start at $321,400 and $160,700, respectively.

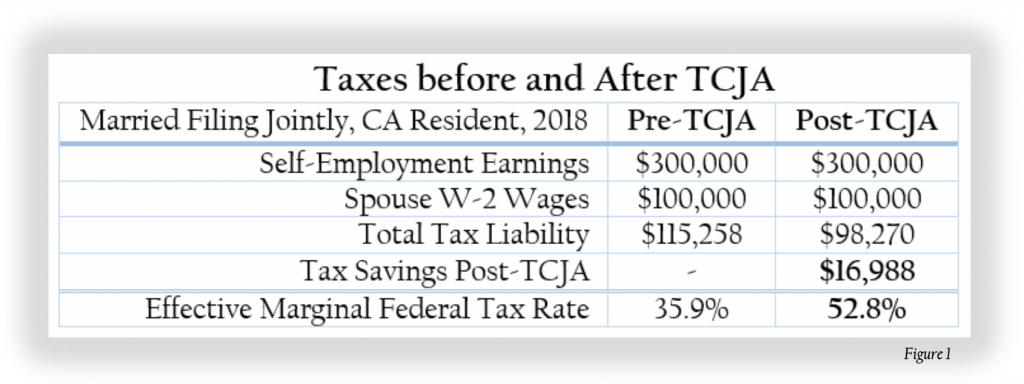

Deduction phase-outs can produce unanticipated, and sometimes nasty tax effects. For example, consider a California couple earning a $400,000 a year, with $300,000 of that coming from self-employment. While the TCJA reduced their overall tax liability by almost $17,000, the QBI phase-out creates an effective federal marginal tax rate of 52.8%. Add in California’s 10.5% effective rate, and this couple faces a combined 63.3% effective marginal tax rate![i]

So while the TCJA reduced this couple’s 2018 tax liability by $16,988, the QBI deduction phase-out, along with California taxes, conspire to create an effective marginal tax rate almost twice the 32% federal bracket they would otherwise find themselves in!

Nevertheless, there’s great possibility for those who know where to look – as the new QBI deduction phase-out itself can offer some self-employed professionals[ii] the opportunity to turn their taxes into savings and investment.

For example, our couple could use their post-TCJA tax refund to make a pre-tax retirement plan contribution. Self-employed professionals have access to an array of different pre-tax retirement plan options, including SIMPLE, Sep-IRA, Individual 401(k), Profit Sharing and even cash balance Defined Benefit plans. There’s no shortage of plans available for the self-employed.

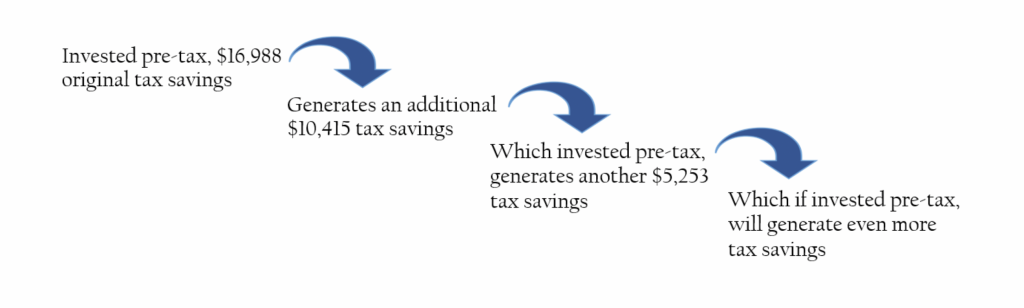

Invested pre-tax, a $16,988 refund would generate another $10,415 in 2018 tax savings! That’s right. While 40, 50 and even 60-plus-percent effective tax rates can be a consequence the new QBI deduction phase-out, those same tax rates reward quite handsomely self-employed professionals able to take advantage of pre-tax retirement savings.

But why stop there? Why stop at generating an additional $10,415 when re-investing that additional tax savings would yield another $5,253 tax break. In other words, by investing the original $16,988 pre-tax, we’re able to generate additional tax savings. And by reinvesting the additional tax savings, we can create even more tax savings – which if reinvested, in turn can create even more additional tax savings.

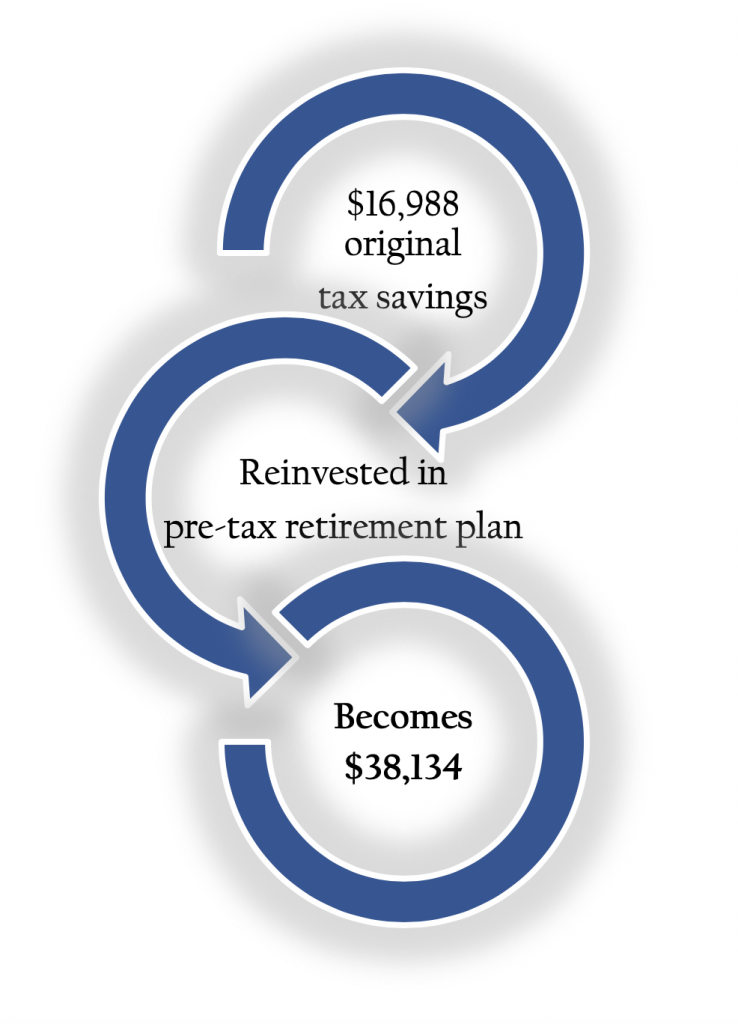

So far, we’ve taken an original tax refund of $16,988 and turned it into a retirement plan contribution of $32,656. But in this example you can, and probably should, rinse and repeat this reinvest-the-tax-savings–in-order-to-generate- more-tax-savings-to-reinvest strategy all the way up to $38,134 before you run out of incrementally generated tax savings to reinvest.

“Most financial planners create financial plans. We create financial possibility.”

Turning $16,988 of TCJA tax savings into $38,134 of retirement plan contributions might feel like creating money to fund retirement out of thin air. That’s because in a way, it is!

Most financial planners create financial plans. We create financial possibility. Debt and taxes tend to make up a disproportionate amount of household expense. But the new Tax Cut and Jobs Act is helping us turn even more Debt & Taxes into Savings & Investment™ for the self-employed.

Too often people fear that to achieve their financial goals they’ll be forced to tighten their belt, cut back on doing the things they love, or simply go without. Many hesitate to hire a financial planner because they don’t even know what’s possible. We’re here to change all that.

If you think our unique approach can help, please let us know. We’d be honored to serve you.

[i] Effective marginal tax rates refer to the tax rate paid on the next $1,000 of taxable income.

[ii]Taxpayers with only QBI income may find their taxable income limits their QBI deduction. The opportunity described above is therefore most applicable where W-2 wages are also present.

My father was fifty-one when he died of cancer. And with the exception of a house, a mortgage, and a little life savings – he died penniless.

Dad loved to fly. He became a flight instructor to help pay for his hobby, as a way to spend more time in the sky. He would share his love of flight with anyone. He’d charge only what he thought you could afford, but the truth is, he’d have done it for free.

There was only one thing dad loved more than flying: His boys. He made huge sacrifices for me and my brother. He sold his airplane to help pay for college and insisted that we get our degrees. He would have liked to fly every day, but put his dreams on hold until we could finish school.

He talked about downsizing his home in order to afford an amphibious aircraft, something he could land on a lake he might call home. He was going to start saving for retirement as soon as we were out of school. He just never got the chance.

It didn’t have to be that way.

The irony is that my father’s sacrifices provided me with the education, training and set of transferable skills that could have saved him the sacrifice in the first place. I could have readily shown him how to put his kids through school, save for the home on the lake, purchase his dream aircraft and retire comfortably. The kicker is, he might even have been able to do so without changing his standard of living or the amount of money he got to spend every month.

I do not believe people should have to struggle financially simply because they cannot throw a 98 mile-an-hour fastball or star in this years’ Academy Award winning film. I believe that people just like my dad can send their children to college, retire early and debt free with well over a million dollars in retirement savings. And I believe they can do it on a middle income wage earner’s salary.

Most of what appears above I wrote more than 20 years ago – a few years aftermy dad passed. I never shared it, never made it public, never completed it until now. But I came across it recently and realized that what I had (merely) believed back then, I can point to now.

I have evidence.

Evidence you don’t have to struggle financially. That you can put your kids through college, retire debt-free, and become a millionaire. And evidence that those skillsare indeed transferable.

I recently became a private pilot myself. And as I was going through the training I got to thinking, no one would ever think you learn to fly an airplane in your head. As if you take a class, pass a final exam, and then some bloke hands you the keys and says “okay, have at it.”

We all recognize you don’t learn to fly an airplane in your head – with knowledge, and information. You learn how to fly an airplane in your body – with skills, and with sensibilities.

Yet when it comes to personal finance, too often we often we retreat back into our heads. Traditional financial planning leans heavily on knowledge and information, relying on probability analysis and predictive algorithms to pre-determine the path to achieving ones financial life goals.

But the world doesn’t work that way. The future has always been uncertain. And the speed and complexity of today’s change is leaving many Americans behind – disoriented and struggling to cope.

What worked in the past is no longer adequate. And knowledge and information, once stable sources of economic power, are no longer enough.

What is needed is a radical reinterpretation of financial planning

This orientation towards prediction and probability is at the root of the problem we see with traditional financial planning. In our view of financial planning, skills matter. And because new skills make available new possibility, our primary aim is to help clients cultivate the personal financial skills and sensibilities necessary not just to cope, but to thrive in a world of uncertainty.

If life were merely random there’d be no point in cultivating new skills. And no reason to engage in our brand of financial planning. Your possibilities would be defined by your probabilities. On the other hand when nothing is certain, far more is possible. It’s in this spirit of uncertain adventure that we engage with you in conversations for possibility, for co-creating your future, and for reinventing your financial reality. Call us, and let’s discover what’s possible for your unique financial situation.

Too often I believe, people hesitate to hire a Certified Financial Planner™ professional because they don’t even know what’s possible.

One of the reasons we don’t see possibility is that we tend to focus on things, like money; debt; investments; or taxes – and not on the relationships that make these things possible in the first place.

Take the phenomenon horizon as an example. Yes horizon, that thing that exists between the earth and the sky.

That thing that quite literally doesn’t exist except in relationship between the earth and the sky.

Without that relationship, there is no there there!

Financial planning isn’t merely about things like stocks, bonds and mutual funds. And it isn’t about blue prints, road maps, or even financial plans.

It isn’t about things at all!

Financial planning is about relationships – and cultivating the skills necessary to navigate life’s uncertainty.

“In preparing for battle I have always found that plansare useless, but planning is indispensable.”

Dwight D. Eisenhower

We live our lives in a world of uncertainty – never knowing what the future will bring. We can’t possible know. And no amount of knowledge, information, calculation, or analysis is going to predict what is fundamentally unpredictable.

Knowledge is useful, but only where knowing is possible. To navigate effectively in today’s world of uncertainty we need more than just knowledge and information. We need skills, and we need sensibilities.

And for that we need to start treating money, debt, investments and taxes less like things and more like the relationships that they are!

Those who insist on treating money like an object; debt as an inherently bad thing; investments like a crap shoot; or taxes as if they’re certain, are headed down a narrow, fixed, rigid, possibilities-constrained dead end road.

The road to possibility isn’t narrow, and it’s certainly not fixed or rigid. It may be paved with good intentions – but only if those intentions are to cultivate the skills and sensibilities to navigate and embrace life’s uncertainty.

Because when nothing is certain, far more is possible.

It’s in this spirit of uncertain adventure that we engage our clients in conversations for possibility, for navigating uncertainty, and for co-creating the future.

By cultivating new skills and sensibilities relating to money, debt, investment and taxes, our clients are reinventing their financial reality.

Psychologist Daniel Kahneman is considered by many in my profession be the father of behavioral economics. In 2002 he was awarded the Nobel Prize in Economic Sciences “for having integrated insights from psychological research into economic science, especially concerning human judgment and decision-making under uncertainty.”

His bestselling book Thinking, Fast and Slow summarizes decades of research, and challenges the assumption of human rationality still prevalent today in many economic theories.

And yet in many ways he is still part of the same rationalistic tradition that believes that when solving complex problems, a detached, unbiased, calculated approach to decision making always leads to the best outcomes.

Intuition and mental shortcuts called heuristics, are the quick and easy way we make decisions in what Kahneman calls System 1 thinking. This is the place where we make decisions by the seat of our pants; emotionally; using our gut. System 2 on the other hand is where reasoning happens; where we make rational decisions; where we slow down, and take a calculated approach.

The problem, according to Kahneman, happens when we try to use System 1 to solve a System 2 problem.

Take the problem “2 + 2,” or “25 x 10.” We can easily solve these kinds of problems without ever reaching for a calculator. It’s a simple, System 1 problem.

Now try “164 divided by π, times the square root of 56.” Here we know well enough to use System 2 and so we do reach for that calculator.

But watch what happens when we mistake a complex System 2 problem for a simple System 1 solution:

Kahneman’s famous example is this:

“A bat and a ball together cost $1.10. The bat costs $1 more than the ball.”

How much does the ball cost?

Most instinctively say “10 cents” – because a dollar-ten separates quite naturally into $1 and 10 cents; and 10 cents seems about right. But it’s not. The right answer takes more calculation. The question, is more complex.

Ultimately the lesson here is clear. When it comes to complex decision making: Listen to your gut, and you will almost always be wrong.

Gerd Gigerenzer thinks this is the wrong lesson. Gigerenzer authoredGut Feelings: The Intelligence of the Unconscious and Rationality for Mortals: How People Cope with Uncertainty. He is director emeritus of the Center for Adaptive Behavior and Cognition at the Max Plank Institute for Human Development. And he’s long been critical of Kahneman’s work.

For example, before applying Kahneman’s System 1 or System 2 – Gigerenzer wants us to first apply this more fundamental, or ontological question:

“Does the problem – that you’re trying to solve – actually, have a solution?”

Because according to Gigerenzer, under conditions of uncertainty, complex problems are better tackled by professionals using trained instinct and expert intuition – than is available by taking an unbiased, detached, rational, calculated, reasoned approach.

The outcomes are simply better.

Answerable problems may well be the province of logic, reason and calculation. The domain of knowledge and information. And fit squarely in the wheelhouse of computers, big data and artificial intelligence. But when it comes to questions that are unanswerable…

The problem with problems is that our clients don’t merely have problems – they have lives!

Lives filed with all the contingency, and uncertainty, and unknown unknowns that

are just part of being, a human being, in the 21st century.

The vast majority of our decisions are not likely to ever become deliberate acts of will. But that doesn’t mean they have to be unreflective acts of irrationality. The good news is it seems we humans have a unique capacity to deal with life’s uncertainty; its unpredictability; even its unknown unknowns.

Besides, if it’s the gut that betrays why bother looking elsewhere? Why not retrain the gut?

Because whether we’re talking about future stock market returns, or the future of climate change and the human race – there are no right answers, only better results.

It’s a common trope among certain types of financial planners: “Save more, spend less… and don’t do anything stupid.” So celebrated is the phrase with some advisers, organizers of a recent conference emblazoned it across baseball caps – attendees proudly wearing the hats as if they were at a MAGA rally.

Beyond the condescending tone and hyperbole however, lies a particular kind of Wall Street fear mongering: Americans of all stripes are facing a looming retirement crisis to which there is no alternative. Cut out your lattes and other discretionary spending or you are destined for destitute. But don’t worry, we’re here to help – just buy our stocks, bonds and annuities.

There’s little doubt that in the aggregate, American’s need to save more. A Boston College survey reports that American’s face a $7.7 trillion retirement income deficit[i] – the difference between what we now have saved, and what we should have savedby now.

But unless you consider debt and taxes to be spending, saving more doesn’t require you to spend less.

Together, we Americans owe almost $14 trillion in combined household debt[ii] and pay over $2 trillion each year in state and federal income taxes.[iii]

If only there were a way to turn Debt & Taxes into Savings & Investment.™

Transforming debt and/or taxes into savings opens the possibility to keep our lattes. And what’s more, save adequately for retirement while spending more, rather than less on the many other things we care about.

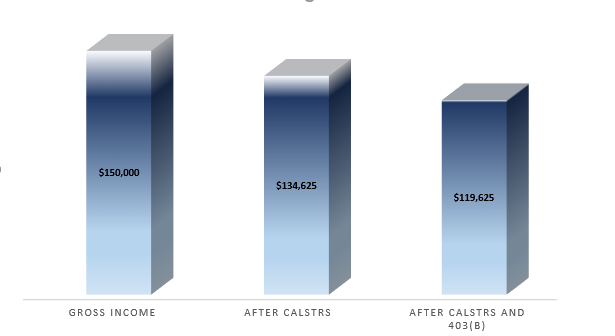

That’s because the very act of savings means not spending that same income. Consider for the moment a married couple, California educators earning a combined $150,000 a year. At first glance it might appear that this couple will eventually need to replace their $150,000/year earnings. Yet further investigation reveals that as California State Teachers’ Retirement System (CalSTRS) members, their gross paychecks are already reduced by 10.25% – the employee’s contribution to the retirement system.

That means our couple lives not off $150,000 of gross income, but less than $135,000 – as more than $15,000 a year is “saved” towards retirement.

And watch what happens to their retirement income needs if our CalSTRS couple starts saving 10% of their income via pre-tax 403(b) contributions:

This simple accounting exercise paints the picture Wall Street doesn’t want you to see, for:

The more you save, the less you need to save for.

And it’s not just $30,375 (the difference between $150,000 and $119,625 in our example) that doesn’t need to be saved for, it’s that difference adjusted for future inflation. Meaning that if inflation runs just 3% over the next 15 years, today’s $30,375 difference is tomorrow’s $45,945 that doesn’t need to be saved for.

Not having to replace $45,000 is like not having to have $1M saved for retirement – because a million dollars is roughly the amount it takes to generate $45,000 a year of sustained retirement income.

Of course if the more your save, the less you need to save for – it follows that the less you need to save for, the more you can spend.

But wait. Hold on a minute. Doesn’t that mean the more you save, the more you can spend?

Yes! Indeed it does!

What initial appears to be a paradox, is actually a fundamental accounting truth:

· The more you save, the less you need to save for.

· The less you need to save, the more you can spend.

This leads to the paradox:

· The more you save, the more you can spend.

But this only looks like a paradox because we tend to think of savings as coming from (i.e. “out of”) spending. But when savings & investment come not at the expense of spending, but at the expense of debt and taxes – existing spending is spared and the paradox disappears.

And along with it any fear and loathing associated with “save more, spend less… and don’t do anything stupid.”

Turning Debt & Taxes into Savings & Investment allows you to Save More, Have More andSpend More.™

Often, more than you ever thought possible.

[i]Center for Retirement Research at Boston College