“It’s the economy, stupid” is a phrase widely used during Bill Clinton’s 1992 presidential campaign. Generally attributed to Clinton political strategist James Carville, the phrase is often repeated in American political culture, with commentators sometimes using a different word in place of “economy”. But whether it’s the deficit, the voters, or the environment(stupid!) you substitute for economy, the phrase is meant to focus attention upon what matters most in the world of politics.

Retirement needs are so often expressed in terms of income (with many experts recommending replacing 70-80% of ones pre-retirement income), you might think income is what matters most in the world of retirement planning.

Unfortunately, this can lead people to conflate income with spending, and the mistaken belief that 70-80% of pre-retirement income is recommended because a 20-30% decline in post-retirement spending is the norm.

What the rule of thumb is actually attempting to convey is the average amount of pre-retirement income not being used to fund pre-retirement spending.

While some pre-retirement income is spent on things like clothing, dry cleaning or commuting expenses – post paycheck spending that will be reduced, or even vanish in retirement – these kinds of expenses tend to be minor compared to payroll deductions like 401(k) contributions, pension obligations, and Social Security taxes.

All of this is to say that the recommendation to replace 70-80% of pre-retirement income is not meant to suggest your post-retirement spending will be any less than it is today.

In fact, hopefully your post-retirement spending on things like food, utilities, entertainment, etc., is every bit as much as it was before you retired!

Who wants to limit their consumption of food, utilities or entertainment to 70-80% of what it was before retirement? In assessing your retirement needs it’s best to target (100% of) your spending rather than (70-80% of) your income. Because when it comes to retirement planning – it’s the spending, stupid!

Working for yourself has its perks. In theory there’s more autonomy when you’re calling the shots. But that autonomy often comes at a cost. Taxes can be particularly burdensome on the self-employed. And the recent Tax Cut and Jobs Act of 2017 (TCJA) re-shuffles the deck on many age-old tax strategies. Navigating the effects of the TCJA is something everyone will need to do. But for self-employed professionals, TCJA offers both threat and opportunity.

The TCJA created a new species of taxpaying entity known as a Specific Service Trade or Business (SSTB). Along with a new category of income called Qualified Business Income (QBI), and corresponding QBI deduction.

Unfortunately for most SSTBs, this new QBI deduction begins to be phased-out for married filers at 2018 taxable incomes of $315,000 ($157,500 for single filers). For 2019, these phase-outs start at $321,400 and $160,700, respectively.

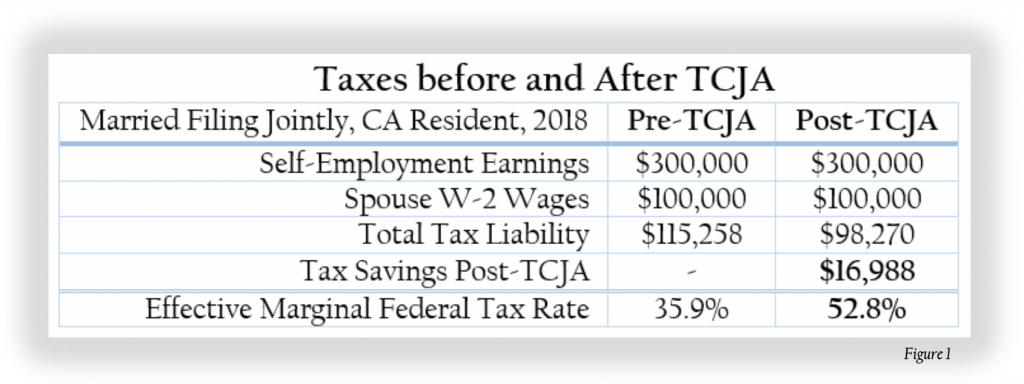

Deduction phase-outs can produce unanticipated, and sometimes nasty tax effects. For example, consider a California couple earning a $400,000 a year, with $300,000 of that coming from self-employment. While the TCJA reduced their overall tax liability by almost $17,000, the QBI phase-out creates an effective federal marginal tax rate of 52.8%. Add in California’s 10.5% effective rate, and this couple faces a combined 63.3% effective marginal tax rate![i]

So while the TCJA reduced this couple’s 2018 tax liability by $16,988, the QBI deduction phase-out, along with California taxes, conspire to create an effective marginal tax rate almost twice the 32% federal bracket they would otherwise find themselves in!

Nevertheless, there’s great possibility for those who know where to look – as the new QBI deduction phase-out itself can offer some self-employed professionals[ii] the opportunity to turn their taxes into savings and investment.

For example, our couple could use their post-TCJA tax refund to make a pre-tax retirement plan contribution. Self-employed professionals have access to an array of different pre-tax retirement plan options, including SIMPLE, Sep-IRA, Individual 401(k), Profit Sharing and even cash balance Defined Benefit plans. There’s no shortage of plans available for the self-employed.

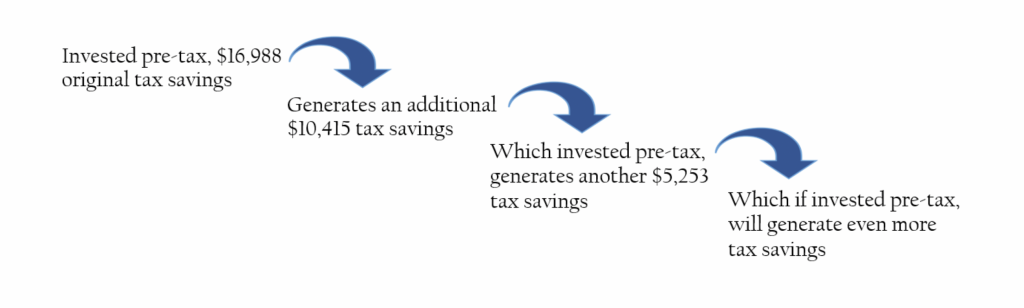

Invested pre-tax, a $16,988 refund would generate another $10,415 in 2018 tax savings! That’s right. While 40, 50 and even 60-plus-percent effective tax rates can be a consequence the new QBI deduction phase-out, those same tax rates reward quite handsomely self-employed professionals able to take advantage of pre-tax retirement savings.

But why stop there? Why stop at generating an additional $10,415 when re-investing that additional tax savings would yield another $5,253 tax break. In other words, by investing the original $16,988 pre-tax, we’re able to generate additional tax savings. And by reinvesting the additional tax savings, we can create even more tax savings – which if reinvested, in turn can create even more additional tax savings.

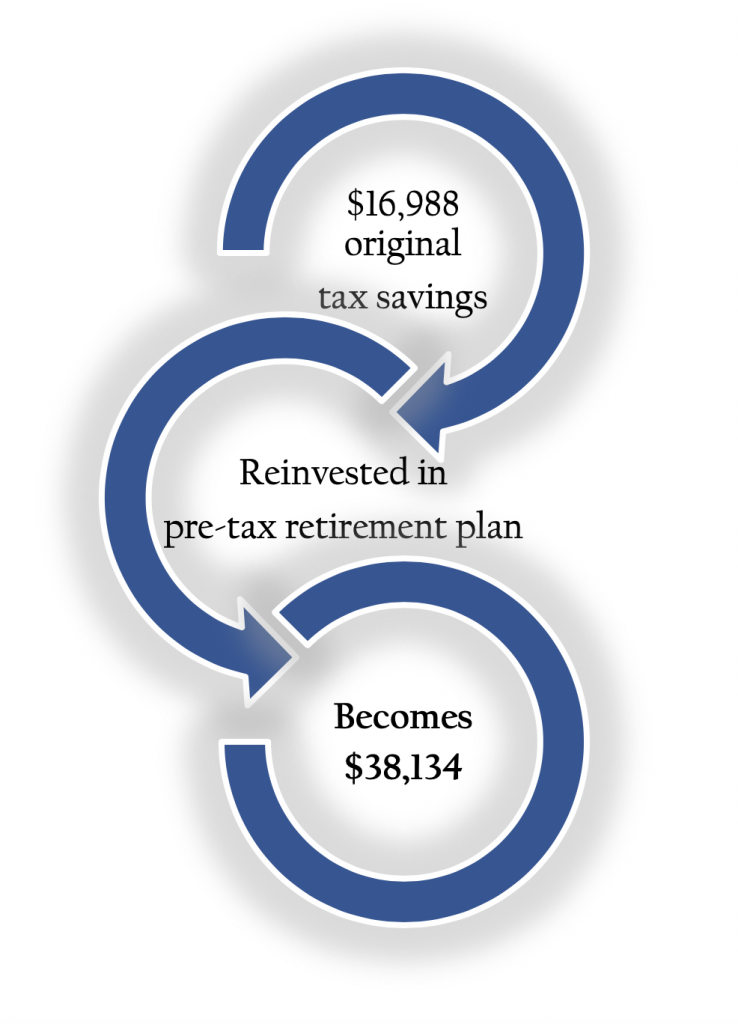

So far, we’ve taken an original tax refund of $16,988 and turned it into a retirement plan contribution of $32,656. But in this example you can, and probably should, rinse and repeat this reinvest-the-tax-savings–in-order-to-generate- more-tax-savings-to-reinvest strategy all the way up to $38,134 before you run out of incrementally generated tax savings to reinvest.

“Most financial planners create financial plans. We create financial possibility.”

Turning $16,988 of TCJA tax savings into $38,134 of retirement plan contributions might feel like creating money to fund retirement out of thin air. That’s because in a way, it is!

Most financial planners create financial plans. We create financial possibility. Debt and taxes tend to make up a disproportionate amount of household expense. But the new Tax Cut and Jobs Act is helping us turn even more Debt & Taxes into Savings & Investment™ for the self-employed.

Too often people fear that to achieve their financial goals they’ll be forced to tighten their belt, cut back on doing the things they love, or simply go without. Many hesitate to hire a financial planner because they don’t even know what’s possible. We’re here to change all that.

If you think our unique approach can help, please let us know. We’d be honored to serve you.

[i] Effective marginal tax rates refer to the tax rate paid on the next $1,000 of taxable income.

[ii]Taxpayers with only QBI income may find their taxable income limits their QBI deduction. The opportunity described above is therefore most applicable where W-2 wages are also present.

My father was fifty-one when he died of cancer. And with the exception of a house, a mortgage, and a little life savings – he died penniless.

Dad loved to fly. He became a flight instructor to help pay for his hobby, as a way to spend more time in the sky. He would share his love of flight with anyone. He’d charge only what he thought you could afford, but the truth is, he’d have done it for free.

There was only one thing dad loved more than flying: His boys. He made huge sacrifices for me and my brother. He sold his airplane to help pay for college and insisted that we get our degrees. He would have liked to fly every day, but put his dreams on hold until we could finish school.

He talked about downsizing his home in order to afford an amphibious aircraft, something he could land on a lake he might call home. He was going to start saving for retirement as soon as we were out of school. He just never got the chance.

It didn’t have to be that way.

The irony is that my father’s sacrifices provided me with the education, training and set of transferable skills that could have saved him the sacrifice in the first place. I could have readily shown him how to put his kids through school, save for the home on the lake, purchase his dream aircraft and retire comfortably. The kicker is, he might even have been able to do so without changing his standard of living or the amount of money he got to spend every month.

I do not believe people should have to struggle financially simply because they cannot throw a 98 mile-an-hour fastball or star in this years’ Academy Award winning film. I believe that people just like my dad can send their children to college, retire early and debt free with well over a million dollars in retirement savings. And I believe they can do it on a middle income wage earner’s salary.

Most of what appears above I wrote more than 20 years ago – a few years aftermy dad passed. I never shared it, never made it public, never completed it until now. But I came across it recently and realized that what I had (merely) believed back then, I can point to now.

I have evidence.

Evidence you don’t have to struggle financially. That you can put your kids through college, retire debt-free, and become a millionaire. And evidence that those skillsare indeed transferable.

I recently became a private pilot myself. And as I was going through the training I got to thinking, no one would ever think you learn to fly an airplane in your head. As if you take a class, pass a final exam, and then some bloke hands you the keys and says “okay, have at it.”

We all recognize you don’t learn to fly an airplane in your head – with knowledge, and information. You learn how to fly an airplane in your body – with skills, and with sensibilities.

Yet when it comes to personal finance, too often we often we retreat back into our heads. Traditional financial planning leans heavily on knowledge and information, relying on probability analysis and predictive algorithms to pre-determine the path to achieving ones financial life goals.

But the world doesn’t work that way. The future has always been uncertain. And the speed and complexity of today’s change is leaving many Americans behind – disoriented and struggling to cope.

What worked in the past is no longer adequate. And knowledge and information, once stable sources of economic power, are no longer enough.

What is needed is a radical reinterpretation of financial planning

This orientation towards prediction and probability is at the root of the problem we see with traditional financial planning. In our view of financial planning, skills matter. And because new skills make available new possibility, our primary aim is to help clients cultivate the personal financial skills and sensibilities necessary not just to cope, but to thrive in a world of uncertainty.

If life were merely random there’d be no point in cultivating new skills. And no reason to engage in our brand of financial planning. Your possibilities would be defined by your probabilities. On the other hand when nothing is certain, far more is possible. It’s in this spirit of uncertain adventure that we engage with you in conversations for possibility, for co-creating your future, and for reinventing your financial reality. Call us, and let’s discover what’s possible for your unique financial situation.

Pre’tire’ment

/prƏti(Ə))rmƏnt/

noun

1. The time of transition from “working too much” to “making work optional.”